This is the sixth and final post in a series on the National Audit Office’s recent report: Outcome-based payment schemes: government’s use of payment by results. The report’s overall conclusion is that because of the lack of a clear evidence base, the PbR approach is currently laden with risk.

A payment by results toolkit

Alongside its recent report on payment by results, the National Audit Office published a “PbR analytical framework for decision-makers” – in effect a toolkit which summarises the contents of the report in a way that commissioners can work through when they are deciding whether to use a PbR approach.

The toolkit has five components:

- Claimed benefits of PbR.

- Structure of PbR schemes.

- Features of public services to which PbR is best suited.

- Risks and challenges of using PbR.

- Framework of questions for commissioners to consider at four key stages.

The full framework covers 8 pages in the report and sets out key questions for commissioners to consider at each of these stages. I have already covered these questions on the previous posts in this series relating to the selection, design, implementation and evaluation of PbR schemes.

[divider]

High level themes

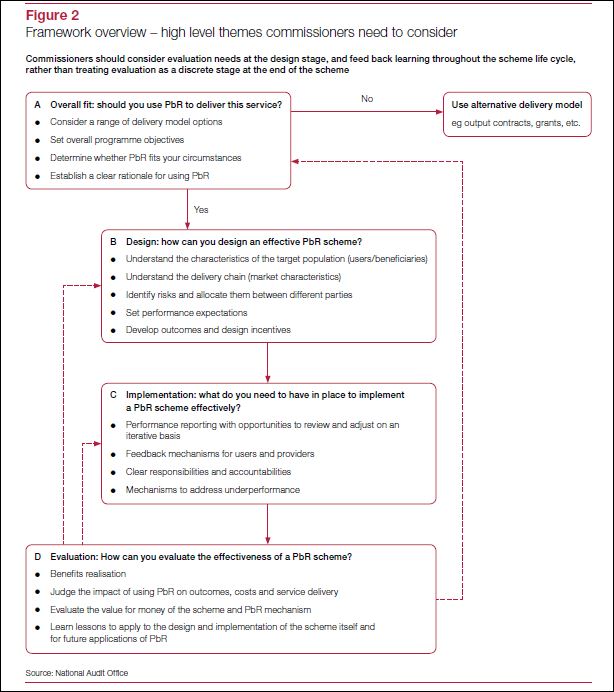

However, the NAO recommends that before looking at these stages in detail, commissioners should consider them in principle first, looking at the full commissioning cycle before deciding whether a PbR approach is appropriate.

The NAO summarises this approach by means of a framework overview which functions as a flowchart and is reproduced below:

Conclusion

Like many of us, the NAO is in a slightly awkward position in regards to payment by results. On the one hand, it is reluctant to recommend that any public programme adopts a PbR approach because there does not, as yet, exist an evidence base that suggests it is an effective commissioning approach.

On the other hand, the NAO acknowledges that over £15 billion of government contracts are let on a PbR approach and therefore wants to provide the best possible guidance to commissioners (and providers) utilising it.

Perhaps the biggest difference between this NAO PbR report and its predecessor (produced in 2012 by the Audit Commission) is the tone of the two documents. Whilst the original report was open-minded about the potential positives of commissioning public services on a payment by results basis, the current document is much more sceptical.